Policy Actions Improve Prospects for Global Economy

IMF Survey online - April 16, 2013

By Thomas Helbling

IMF Research Department

- IMF projects global growth at 3.3 percent in 2013, up to 4 percent in 2014

- Recovery uneven in advanced economies; private demand in United States improving faster than in euro area

- Developing, emerging economies persist in leading global growth

The global economy is expected to continue mending gradually, says the International Monetary Fund (IMF), whose latest forecast of economic growth projects 3.3 percent growth in 2013, and 4 percent in 2014. But with old dangers remaining and new risks emerging, policymakers cannot afford to relax their efforts.

Global economic conditions have improved during the past six months. Advanced economy policymakers successfully defused two of the biggest short-term risks to global activity—the threat of a euro area breakup and a sharp fiscal contraction in the United States. Financial markets have rallied in response, and financial stability has improved, according to the IMF’s latest World Economic Outlook (WEO).

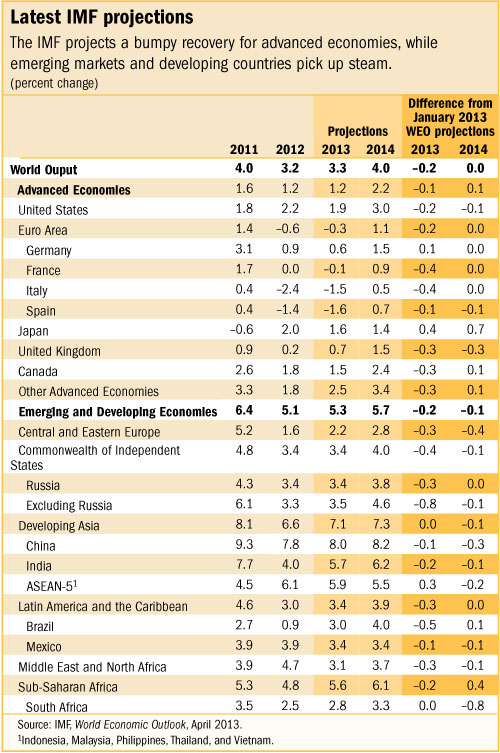

The report forecasts real global GDP growth of 3.3 percent on an annual average basis in 2013, about the same as the 3.2 percent growth seen in 2012, and the IMF expects growth to rise to 4 percent in 2014 (see table below). The WEO says the main reason behind the broadly unchanged growth prospects this year is that advanced economies have not all benefited to the same extent from the improved financial market conditions and confidence. Fiscal brakes in some countries were another important factor.

“We have moved from a two-speed recovery to a three-speed recovery,” said Olivier Blanchard, the IMF’s chief economist and director of the IMF’s Research Department, which prepares the WEO. “Emerging market and developing economies are still going strong, but in advanced economies, there appears to be a growing bifurcation between the United States on the one hand and the euro area on the other.”

• Private demand in the United States has been showing strength as credit and housing markets heal. But larger-than-expected fiscal adjustment is projected to keep real GDP growth to about 2 percent in 2013.

• In the euro area, real GDP is projected to contract by about ¼ percent this year before growing again in 2014. Credit channels are broken: better financial conditions are not yet passing through to companies and households because banks are still hobbled by poor profitability and low capital. Other brakes on growth in the euro area include continued fiscal adjustment, competitiveness problems, and balance sheet weaknesses.

• In Japan, new fiscal and monetary stimulus is expected to drive a rebound in activity, with real GDP growth reaching 1½ percent in 2013.

Over 2013–14, these divergences between advanced economies are projected to narrow. Assuming that policymakers deliver on their commitments, the latest WEO report anticipates continued easing of the brakes on real activity and a strengthening of real GDP growth in the advanced economies from the second half of 2013.

Growth in emerging market and developing economies is expected to remain robust, strengthening from about 5 percent in 2012 to 5¼ percent in 2013 and 5¾ percent in 2014. Activity in most of these economies has already picked up after a slowdown in 2012, thanks to resilient consumer demand, supportive macroeconomic policies, and a revival of exports. In emerging Europe, the recovery should gain speed as demand from advanced economies in Europe picks up. However, some economies in the Middle East and North Africa continue to struggle with difficult internal transitions.

Improvements in the balance of risks

The WEO observes that recent policy actions in Europe and the United States have improved the short-term risk picture although dangers are still present. In the euro area, the recovery could be slower than expected because of adjustment fatigue, weak balance sheets, broken credit channels in the periphery, and insufficient progress toward stronger economic and monetary union. In the United States, larger-than-expected fiscal adjustment from automatic spending cuts (the so-called budget sequester) or failure to raise the debt ceiling could exert a stronger drag on growth.

Over the medium term, however, the balance of risks remains on the downside. Concerns revolve around the absence of strong fiscal consolidation plans in the United States and Japan; high private sector debt, limited policy space, and insufficient institutional progress in the euro area, which could lead to a protracted period of low growth; distortions from easy and unconventional monetary policy in major advanced economies; and overinvestment and high asset prices in many emerging market and developing economies.

Stabilization requirement for robust growth

In the face of these risks, the report underscores, policymakers cannot relax their efforts. Risks from high sovereign debt generally limit the fiscal policy room for maneuver in most advanced economies, and fiscal adjustment must progress gradually to limit damage to demand in the short term. Monetary policy therefore must remain supportive of private demand, while financial policies need to help improve the pass-through of monetary policy. The United States and Japan have yet to design and implement comprehensive medium-term deficit-reduction plans. This is an urgent requirement for Japan, given the significant risks from renewed fiscal stimulus combined with very high public debt levels. Structural reforms to rebuild competitiveness and boost medium-term growth prospects are critical for many euro area economies, as is further progress on architecture reforms to complete the economic union.

In emerging market and developing economies, the WEO highlights the need to tighten policies and rebuild buffers. The tightening should begin with monetary policy and, when needed, be supported with prudential measures to rein in budding excesses in financial sectors. And fiscal balances should be returned to levels that afford ample room (“buffers”) for policy maneuver should growth fall below trend in the future.