Russian

(pdf)

Fiscal Monitor Update

Nurturing Credibility While Managing Risks

to Growth

July 16, 2012

Download

PDF

Fiscal adjustment is proceeding generally as expected in

advanced economies, with headline and underlying fiscal deficits

that are broadly in line with projections in the April 2012

Fiscal Monitor. Overall, advanced economy deficits are

forecast to decline by about ¾ percentage point of GDP this year

and about 1 percent of GDP next year in both headline and

cyclically adjusted terms, a rate that strikes a compromise

between restoring fiscal sustainability and supporting growth.

However, continued focus on nominal deficit targets runs the

risk of compelling excessive fiscal tightening if growth

weakens. In addition, there is a risk in the United States of

political gridlock that puts fiscal policy on autopilot and

results in a sharp and sudden decline in deficits—the “fiscal

cliff.” In most advanced economies, a steady pace of adjustment

focused on the measures to be implemented rather than on

headline deficit targets is preferable, especially in light of

heightened downside risks to the outlook. In most emerging

economies, headline and cyclically adjusted deficits are

projected to remain broadly unchanged over 2012–13, which is

appropriate given these countries’ generally stronger fiscal

positions and the downside risks to the global economy. However,

some emerging economies need to be more ambitious to reduce

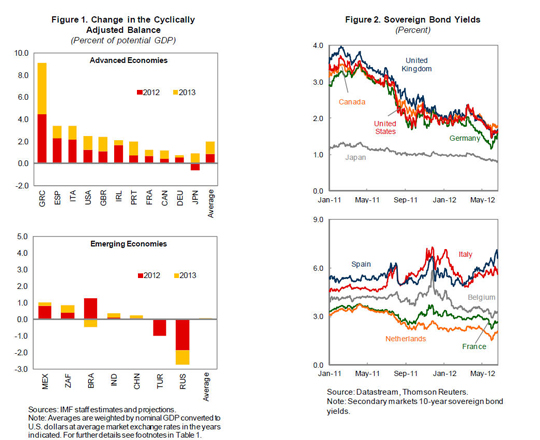

vulnerabilities.Underlying fiscal adjustment on track

Fiscal imbalances are being gradually corrected in line with

expectations in most advanced economies. Cyclically adjusted

deficits in 2012–13 are expected to fall by close to 1 percent

of GDP annually on average in advanced economies—about the same

amount as last year and broadly as projected in the April 2012

Fiscal Monitor—with greater reductions in countries

under market pressure (Table 1, Figure 1).

The two largest such countries are implementing sizeable

fiscal consolidation in the next two years in efforts to improve

debt dynamics and regain market confidence.

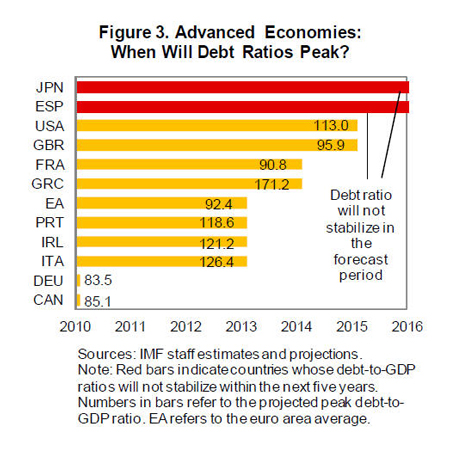

- Market turbulence has intensified in Spain due

to renewed concerns about the health of the financial system

and its possible fiscal implications (Figure 2). Despite an

ambitious and largely expenditure-based consolidation

package, revenue underperformance due to the recession and

higher spending pressures from unemployment insurance costs,

social security outlays and interest payments were expected

to push the deficit close to 7 percent of GDP this year

before the announcement of new measures on July 11. This is

about 1 percent of GDP more than projected in April, but

still about 2 percentage points of GDP below last year’s

outturn. The cyclically adjusted deficit projection had also

been revised up. This may reflect factors that are leading

to a temporary increase in the sensitivity of the budget

balance to output. Deficit targets have been revised to

6.3 percent of GDP this year and 4.5 percent of GDP next

year under the EU’s Excessive Deficit Procedure.

|

|

|

Table 1. Fiscal Indicators, 2008–13 |

|

(Percent of GDP, except where otherwise noted) |

|

| |

|

|

|

Est. |

Projections |

|

Difference from April 2012 Fiscal Monitor1 |

|

|

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

|

2011 |

2012 |

2013 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Overall Fiscal Balance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Advanced economies |

-3.5 |

-8.8 |

-7.6 |

-6.5 |

-5.8 |

-4.7 |

|

0.0 |

-0.1 |

-0.2 |

|

United States |

-6.7 |

-13.0 |

-10.5 |

-9.6 |

-8.2 |

-6.8 |

|

0.0 |

-0.1 |

-0.5 |

|

Euro area |

-2.1 |

-6.4 |

-6.2 |

-4.1 |

-3.2 |

-2.5 |

|

0.0 |

0.0 |

0.2 |

|

France |

-3.3 |

-7.6 |

-7.1 |

-5.2 |

-4.5 |

-3.9 |

|

0.1 |

0.1 |

0.0 |

|

Germany |

-0.1 |

-3.2 |

-4.3 |

-1.0 |

-0.7 |

-0.4 |

|

0.0 |

0.1 |

0.2 |

|

Greece2 |

-12.2 |

-15.6 |

-10.5 |

-9.2 |

-7.0 |

-2.7 |

|

0.0 |

0.2 |

1.9 |

|

Ireland |

-7.3 |

-14.0 |

-31.2 |

-13.1 |

-8.3 |

-7.5 |

|

-3.3 |

0.2 |

-0.2 |

|

Italy |

-2.7 |

-5.4 |

-4.5 |

-3.9 |

-2.6 |

-1.5 |

|

0.0 |

-0.2 |

0.1 |

|

Portugal |

-3.7 |

-10.2 |

-9.8 |

-4.2 |

-4.5 |

-3.0 |

|

-0.2 |

0.0 |

0.0 |

|

Spain3 |

-4.5 |

-11.2 |

-9.3 |

-8.9 |

-7.0 |

-5.9 |

|

-0.4 |

-1.0 |

-0.2 |

|

Japan |

-4.1 |

-10.4 |

-9.4 |

-10.1 |

-9.9 |

-8.6 |

|

0.0 |

0.1 |

0.2 |

|

United Kingdom |

-5.0 |

-10.4 |

-9.9 |

-8.6 |

-8.1 |

-7.1 |

|

0.1 |

-0.2 |

-0.5 |

|

Canada |

-0.1 |

-4.9 |

-5.6 |

-4.4 |

-3.8 |

-2.9 |

|

0.2 |

-0.2 |

0.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Emerging economies |

0.2 |

-4.5 |

-3.3 |

-1.7 |

-1.9 |

-2.0 |

|

-0.1 |

-0.3 |

-0.3 |

|

China |

-0.4 |

-3.1 |

-2.3 |

-1.2 |

-1.3 |

-1.0 |

|

0.0 |

0.0 |

0.0 |

|

India |

-8.8 |

-9.7 |

-9.4 |

-8.9 |

-8.9 |

-8.8 |

|

-0.2 |

-0.6 |

-0.6 |

|

Russia |

4.9 |

-6.3 |

-3.5 |

1.6 |

0.1 |

-0.7 |

|

0.0 |

-0.5 |

-0.4 |

|

Turkey |

-2.4 |

-5.6 |

-2.7 |

-0.3 |

-1.7 |

-2.0 |

|

0.0 |

0.0 |

0.0 |

|

Brazil |

-1.3 |

-3.0 |

-2.7 |

-2.6 |

-1.9 |

-2.1 |

|

0.0 |

0.5 |

0.3 |

|

Mexico |

-1.1 |

-4.7 |

-4.3 |

-3.4 |

-2.4 |

-2.2 |

|

0.0 |

-0.1 |

-0.1 |

|

South Africa |

-0.5 |

-5.3 |

-4.8 |

-4.5 |

-4.4 |

-3.8 |

|

0.1 |

-0.1 |

-0.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Low-income economies |

-1.0 |

-4.0 |

-2.7 |

-2.4 |

-3.0 |

-2.5 |

|

-0.1 |

-0.1 |

-0.2 |

| |

|

|

|

|

|

|

|

|

|

|

General Government Cyclically Adjusted

Balance

(Percent of potential GDP) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Advanced economies |

-3.8 |

-6.0 |

-6.1 |

-5.4 |

-4.7 |

-3.6 |

|

-0.2 |

-0.2 |

-0.2 |

|

United States4 |

-5.5 |

-7.9 |

-8.1 |

-7.5 |

-6.3 |

-5.0 |

|

-0.4 |

-0.4 |

-0.6 |

|

Euro area |

-3.1 |

-4.5 |

-4.6 |

-3.3 |

-2.0 |

-1.4 |

|

0.0 |

0.0 |

0.1 |

|

France |

-3.1 |

-5.1 |

-5.1 |

-3.8 |

-3.1 |

-2.6 |

|

0.2 |

0.1 |

0.1 |

|

Germany |

-1.3 |

-1.3 |

-3.4 |

-1.2 |

-0.6 |

-0.4 |

|

0.0 |

0.0 |

0.1 |

|

Greece2 |

-16.4 |

-18.5 |

-12.5 |

-9.0 |

-4.5 |

0.2 |

|

-2.2 |

0.1 |

2.9 |

|

Ireland |

-11.9 |

-10.6 |

-9.8 |

-7.7 |

-6.0 |

-5.6 |

|

… |

… |

… |

|

Italy |

-3.3 |

-3.0 |

-3.1 |

-2.7 |

-0.5 |

0.7 |

|

0.0 |

-0.2 |

0.0 |

|

Portugal |

-3.6 |

-8.8 |

-9.1 |

-2.9 |

-2.1 |

-0.9 |

|

-0.2 |

-0.1 |

-0.1 |

|

Spain3 |

-5.6 |

-9.7 |

-7.6 |

-7.3 |

-5.0 |

-3.9 |

|

-0.4 |

-1.1 |

-0.3 |

|

Japan |

-3.5 |

-7.4 |

-7.9 |

-8.2 |

-8.8 |

-7.9 |

|

0.0 |

-0.1 |

0.1 |

|

United Kingdom |

-7.2 |

-9.7 |

-8.4 |

-6.6 |

-5.5 |

-4.2 |

|

-0.3 |

-0.4 |

-0.4 |

|

Canada |

-0.6 |

-2.6 |

-4.1 |

-3.4 |

-3.0 |

-2.2 |

|

0.2 |

-0.2 |

0.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Emerging economies |

-1.5 |

-3.6 |

-3.1 |

-1.9 |

-1.7 |

-1.7 |

|

0.0 |

-0.1 |

0.0 |

|

China |

0.0 |

-2.4 |

-1.5 |

0.0 |

0.0 |

0.2 |

|

0.0 |

0.0 |

0.0 |

|

India |

-8.8 |

-9.8 |

-9.6 |

-9.1 |

-9.0 |

-8.7 |

|

0.0 |

-0.2 |

0.0 |

|

Russia |

3.9 |

-3.3 |

-2.2 |

1.7 |

-0.2 |

-1.1 |

|

0.1 |

-0.4 |

-0.3 |

|

Turkey |

-3.2 |

-4.7 |

-3.4 |

-1.8 |

-2.8 |

-2.8 |

|

0.0 |

0.0 |

0.0 |

|

Brazil |

-2.1 |

-2.2 |

-3.2 |

-2.8 |

-1.5 |

-2.0 |

|

-0.1 |

0.6 |

0.3 |

|

Mexico |

-1.3 |

-3.8 |

-3.9 |

-3.2 |

-2.4 |

-2.2 |

|

0.0 |

-0.1 |

-0.1 |

|

South Africa |

-2.3 |

-5.1 |

-4.5 |

-4.1 |

-3.7 |

-3.3 |

|

0.1 |

-0.1 |

-0.1 |

| |

|

|

|

|

|

|

|

|

|

|

|

General Government Gross Debt |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Advanced economies |

81.6 |

95.4 |

101.5 |

105.6 |

110.0 |

112.2 |

|

0.0 |

0.8 |

1.0 |

|

United States |

76.1 |

89.9 |

98.4 |

102.8 |

106.7 |

110.7 |

|

-0.1 |

0.1 |

0.5 |

|

Euro area |

70.2 |

80.0 |

85.8 |

88.1 |

91.4 |

92.4 |

|

0.0 |

1.4 |

1.4 |

|

France |

68.3 |

79.2 |

82.4 |

86.1 |

88.2 |

90.1 |

|

-0.2 |

-0.9 |

-0.7 |

|

Germany |

66.9 |

74.7 |

83.5 |

81.2 |

82.2 |

80.1 |

|

-0.3 |

3.3 |

2.7 |

|

Greece2 |

112.6 |

129.0 |

144.5 |

165.4 |

162.6 |

171.0 |

|

4.6 |

9.4 |

10.1 |

|

Ireland |

44.2 |

65.1 |

92.5 |

108.2 |

117.6 |

121.2 |

|

3.2 |

4.4 |

3.5 |

|

Italy |

105.8 |

116.1 |

118.7 |

120.1 |

125.8 |

126.4 |

|

0.0 |

2.5 |

2.6 |

|

Portugal |

71.6 |

83.1 |

93.3 |

107.8 |

114.4 |

118.6 |

|

1.0 |

2.0 |

3.3 |

|

Spain3 |

40.2 |

53.9 |

61.2 |

68.5 |

90.3 |

96.5 |

|

0.0 |

11.2 |

12.5 |

|

Japan |

191.8 |

210.2 |

215.3 |

229.9 |

234.5 |

240.0 |

|

0.1 |

-1.3 |

-1.1 |

|

United Kingdom |

52.5 |

68.4 |

75.1 |

82.3 |

88.6 |

92.7 |

|

-0.2 |

0.2 |

1.3 |

|

Canada |

71.1 |

83.6 |

85.1 |

84.7 |

85.4 |

82.7 |

|

-0.3 |

0.7 |

0.8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Emerging economies |

33.3 |

35.4 |

40.1 |

36.4 |

34.2 |

32.7 |

|

0.0 |

0.3 |

0.5 |

|

China |

17.0 |

17.7 |

33.5 |

25.8 |

22.0 |

19.4 |

|

0.0 |

0.0 |

0.0 |

|

India |

75.2 |

72.2 |

67.7 |

67.1 |

68.0 |

68.6 |

|

-1.0 |

0.4 |

1.8 |

|

Russia |

7.9 |

11.3 |

11.8 |

12.0 |

11.5 |

11.3 |

|

2.4 |

3.1 |

3.4 |

|

Turkey |

40.0 |

46.1 |

42.2 |

39.4 |

36.0 |

34.6 |

|

0.0 |

0.0 |

0.0 |

|

Brazil |

63.5 |

66.9 |

65.2 |

64.9 |

64.2 |

61.7 |

|

-1.2 |

-0.9 |

-1.4 |

|

Mexico |

43.1 |

44.5 |

42.9 |

43.8 |

42.7 |

42.9 |

|

0.0 |

-0.1 |

0.0 |

|

South Africa |

27.4 |

31.5 |

35.3 |

38.7 |

40.2 |

41.3 |

|

-0.1 |

0.2 |

0.5 |

|

Low-income countries |

40.8 |

42.5 |

40.2 |

39.3 |

41.6 |

39.7 |

|

0.4 |

0.9 |

0.3 |

| |

|

|

|

|

|

|

|

|

|

|

| Memorandum: |

|

|

|

|

|

|

|

|

|

|

| World Growth (Percent) |

2.8 |

-0.6 |

5.3 |

3.9 |

3.5 |

3.9 |

|

0.0 |

-0.1 |

-0.2 |

|

|

Sources: IMF staff estimates and

projections. Note: All

fiscal data country averages are weighted by nominal

GDP converted to U.S. dollars at average market

exchange rates in the years indicated and based on

data availability. Projections are based on IMF

staff assessment of current policies.

1

For overall fiscal balance and cyclically adjusted

balance, positive values indicate a smaller fiscal

deficit; for gross debt, positive values indicate a

larger debt.

2

For Greece, projections to be revised.

3

For Spain, projections do not reflect the measures

announced on July 11, 2012.

4

Excluding financial sector support. |

|

The new targets, respectively 1 and 1½ percentage points

above the previous ones, appropriately accommodate the weak

growth outlook. On July 11, the government announced a series of

measures—including increases in VAT rates, the elimination of

mortgage interest deductibility under the income tax, and cuts

in civil service pay and unemployment benefits—to help achieve

the new targets. To recapitalize the banking system, Spain’s

bank support fund—Fondo de Reestructuración Ordenada Bancaria (FROB)—is

to have access to a financial sector recapitalization loan by

the European Financial Stability Facility (EFSF) for up to 9

percent of GDP (€100 billion) committed by the Eurogroup, which

would be reflected in the general government gross debt.

However, once a single supervisory system is established in the

euro area, the European Stability Mechanism (ESM) will be

allowed to inject capital directly into the banks.1

- Italy’s headline and cyclically adjusted

deficits for 2012–13 continue to be broadly in line with

expectations. Fiscal adjustment over the next two years

would allow the authorities to achieve a small structural

surplus in 2013 (against the medium-term objective of a

structurally balanced budget2).

This focus on structural fiscal targets is enshrined in a

recently approved constitutional balanced budget rule coming

into force in 2014. The bill amending the Constitution also

mandates the establishment of a fiscal council whose remit

and institutional features will be defined in secondary

legislation currently under discussion. The authorities plan

to use spending reviews more systematically to identify

fiscal savings; a first phase, approved in July, legislates

spending cuts in order to rebalance the earlier fiscal

consolidation package away from tax increases.

In the three euro area countries with programs supported by

EU/IMF lending, adjustment is proceeding, but the recent

deterioration in the political and economic climate in Greece

serves as a warning about the potential onset of “adjustment

fatigue,” which remains a threat to continued program

implementation.

- The situation in Greece remains fluid.

Macroeconomic deterioration and uneven reform implementation

have weighed on revenues this year, while financing

constraints are leading to under-execution of budgeted

expenditures. Absent further policy changes, the primary

deficit would trend towards 1½ to 2 percent of GDP, versus

the 1 percent foreseen at the time of the Extended Fund

Facility (EFF).

- Fiscal adjustment is proceeding as targeted in

Portugal, where the deficit is expected to fall to

4½ and 3 percent of GDP this year and next, respectively,

with this decline to be achieved mainly through expenditure

restraint. The adoption of a medium-term expenditure

framework—with indicative expenditure ceilings—is expected

to strengthen program implementation. The authorities are

also to provide capital injections into three of the largest

banks (amounting to 4 percent of GDP) to meet capital

requirements set by the European Banking Authority,

increasing the ratio of gross debt to GDP (but not the

measured deficit).

- In Ireland, the authorities are on track to

meet the program targets and keep pace with the objective of

reaching the 3 percent of GDP EU threshold for the headline

deficit by 2015.3

The general government deficit target of 8.6 percent of GDP

for 2012 appears likely to be met, especially given the

slightly better than expected fiscal performance through

May.

In advanced economies with easier market access, fiscal

adjustment in 2012–13 is broadly on track to meet medium-term

targets.

- Projected fiscal withdrawal in Germany for 2012

and 2013 is unchanged since April at relatively modest

levels.

- In the United Kingdom, the cyclically adjusted

deficit will continue to decline this year and next, but by

less than last year, which is fitting given the weak growth

outlook. The government has appropriately maintained its

commitments to balance the structural current budget within

five years and to put net debt on a declining path, with

additional consolidation in store in 2015–17.

- In France, the new administration has committed

to reducing its headline deficit by about 1 percent of GDP

this year and 1½ percent of GDP next year to 3 percent of

GDP, in line with earlier projections (with a commitment to

a balanced budget by 2017, a year later than envisaged

earlier).4

With a view to reaching these targets, the supplementary

budget includes new measures of about 0.3 percent of GDP,

mainly on the revenue side, to compensate for revenue

shortfalls. The underlying adjustment implicit in these

targets is appropriate under the baseline scenario. However,

in the event that growth disappoints, these targets could

entail an excessive structural adjustment. Thus a shift to

structural deficit targets could be desirable.

- The United States’ fiscal position is projected

to improve this year (broadly in line with the April 2012

Fiscal Monitor projections), but the outlook for

2013 remains a significant concern.5

Expiring tax provisions (such as income and payroll tax cuts

and limitations on the reach of the Alternative Minimum Tax

through an adjustment of the income threshold) and automatic

spending cuts mandated by the 2011 Budget Control Act would

imply a fiscal withdrawal of more than 4 percent of GDP—the

so-called ‘fiscal cliff’—which would severely affect growth

in the short term.6

A more modest retrenchment in 2013—of around 1 percent of

GDP in structural terms—would be a better option. Early

action on the federal debt ceiling, which is expected to

become binding late this year or early next, would mitigate

risks of financial market disruptions and a loss in consumer

and business confidence.

- Following a political agreement in Japan, the

draft bill to double the consumption tax rate in stages to

10 percent by 2015 passed the lower house in late June and

has been sent to the upper house. This welcome development

sends a positive signal of commitment to fiscal adjustment

and reform. However, the tax increase would remain only part

of the consolidation necessary to put the debt ratio on a

downward path. To support further fiscal consolidation and

mitigate the negative economic impact of the consumption tax

increase, adjustment measures should be complemented by

efforts to raise growth through structural measures,

supportive monetary policy, and fiscally-prudent,

growth-friendly tax and expenditure reforms.

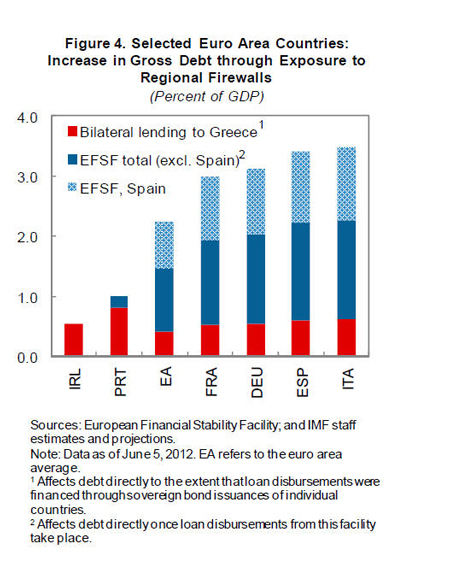

The decline in deficits is gradually affecting public debt

dynamics. While the average debt-to-GDP ratio among advanced

economies is projected to continue to rise over the next two

years, surpassing 110 percent of GDP on average in 2013, debt

ratios will by then have peaked in several advanced economies

(Figure 3). Already this year, about one-third of advanced

economies will have declining debt ratios, although debt ratios

will still exceed their 2007 levels in almost all cases. In the

euro area other than Greece, gross debt dynamics in 2012–13 will

be negatively (and temporarily) affected by the pooling of

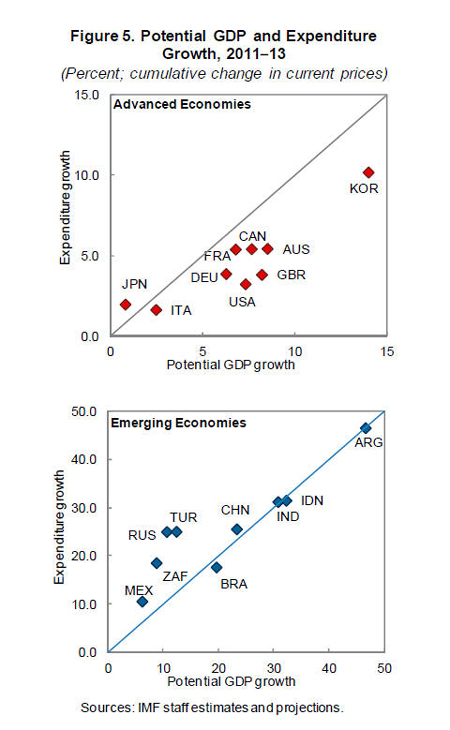

resources to support countries in crisis (Figure 4, box). Of

course, the corresponding acquisition of assets leaves net debts

unchanged.

Deficits in emerging economies are expected to be somewhat

weaker than projected in April, as some draw on fiscal space in

response to slowing economic activity. No significant fiscal

consolidation is on tap in 2012–13, reflecting generally

stronger fiscal positions than in advanced economies and

downside risks to global growth.

- In Brazil, the overall balance for 2012 is

expected to be ½ percent of GDP stronger than envisaged

earlier, mainly on account of lower interest payments.

Despite recently announced measures to support selected

industrial sectors and investment (estimated at about

0.4 percent of GDP), the authorities are still expected to

achieve the 3.1 percent of GDP primary surplus target.

- Fiscal consolidation is projected to advance gradually

in Mexico in 2012–13, in line with earlier

projections. In 2013, the authorities are expected to return

to their balanced budget target.

- In China, fiscal consolidation is expected to

be put on hold this year—which is appropriate in light of

slower growth and a strong fiscal position (headline deficit

of around 1¼ percent of GDP)—before resuming slowly in 2013.

- In South Africa, improving revenue performance

and a gradual withdrawal of fiscal stimulus should

contribute to a decline in the cyclically adjusted fiscal

deficit by 0.9 percent of GDP over the next two years, in

line with earlier projections.

That said, some emerging economies should pursue more

ambitious consolidation strategies, reflecting macroeconomic or

fiscal considerations.

- In Russia, fiscal policy will continue to

exhibit a strong procyclical bent. With oil revenue

windfalls financing expenditure growth, this year’s non-oil

deficit is expected to increase by about 1 percentage point

to 10½ percent of GDP, despite the closing of the output

gap. Meanwhile, the 2012–14 medium-term budget does not

provide for a meaningful improvement in the non-oil deficit,

making public finances highly vulnerable to petroleum market

developments.

- In Turkey, revenue shortfalls related to

slowing activity are expected to increase the overall

deficit by 1½ percent of GDP this year, leaving the

structural primary deficit broadly unchanged. Looking

forward to 2013 and beyond, a tighter fiscal stance seems

appropriate to help reduce the large current account

deficit.

- In India, overall deficits for 2012–13 were

revised upward to almost 9 percent of GDP, more than ½

percentage point higher than in the April 2012 Fiscal

Monitor, mainly due to higher fuel subsidies and

revenue shortfalls. A determined reduction in costly

subsidies would be a strong signal of a credible fiscal

turnaround. It would also allow relaxation of financial

restrictions, spurring private investment and growth.

Reconciling Credibility and Growth

Governments face the task of credibly dealing with large

fiscal adjustment needs in a time of slow and uncertain growth.

Reconciling these needs may be challenging, but following some

basic fiscal principles (to be adapted on a case- by-case basis)

should help:7

Effects of EU Firewalls on Gross Public Debt Ratios

Pooling of resources through the EFSF and

contributions to the paid-in capital of the ESM largely

explain upward revisions to projected gross debt levels

for this year and next compared to the April 2012

Fiscal Monitor in several euro area countries,

notably Germany (3 percentage points of GDP) and Italy

(2½ percentage points).1

EFSF disbursements directly increase gross

liabilities of the countries guaranteeing the EFSF’s

debt in proportion to these countries’ capital shares in

the European Central Bank (ECB) adjusted to exclude

countries with EU/IMF supported programs. Existing loans

represent slightly more than 1 percent of euro area GDP

in mid-2012, with a corresponding increase in EFSF

guarantors’ debt. In the case of Italy and Spain, this

represents 1.6 percent of GDP. The recently announced

financing of the Spanish bank recapitalization will

initially be channeled through an EFSF loan to the

sovereign, increasing the euro area debt by an

additional ¾ percent of GDP. Of course, these additions

to public debts are by nature temporary and matched by

an accumulation of assets.

Because it predates the EFSF, the first Greek program

was largely financed by €80 billion in bilateral loans,

pooled by the European Commission (EC) in proportion to

countries’ ECB capital shares. Disbursements to Greece

amounted to ½ percent of euro area GDP, though loans

provided by Italy, Portugal, and Spain were higher in

proportion to their GDP.

__________________________________

1 A second firewall, the European

Financial Stabilization Mechanism (EFSM), allows the EC

to borrow up to €60 billion on behalf of the European

Union. The corresponding bond issuances do not affect

national public debts. Euro area countries must also

capitalize the ESM, slated to become operational in July

2012 once ratified by national parliaments. The ESM will

have an initial lending capacity of €500 billion and a

total subscribed capital of €700 billion, of which €80

billion will be in the form of paid-in capital to be

phased in with a maximum of five installments. Part of

these capital contributions has already been

incorporated into debt projections, as mentioned

earlier. |

- To anchor market expectations, country authorities need

to specify adequately detailed medium-term plans aimed at

lowering debt ratios and backed by binding legislation or

fiscal frameworks. Among large advanced economies, both the

United States and Japan still lack such plans.

- Within these plans, and to the extent that market

financing remains at sustainable rates, adjustment should

take place at a steady pace defined in cyclically adjusted

terms. On average, an annual pace of adjustment of about 1

percentage point of GDP—as in advanced economies in

2011–13—seems to be broadly adequate in reconciling the need

to address the challenge of fiscal consolidation while

managing risks to growth, although the appropriate pace of

adjustment for each country should reflect the size of the

overall fiscal imbalance. Defining targets in cyclically

adjusted terms allows automatic stabilizers to operate, thus

mitigating possible shocks. In Europe, several countries

have explicitly adopted structural balance targets,

including Germany, Italy, and the United Kingdom, and the EC

has increasingly used the flexibility embedded in the

corrective arm of the Stability and Growth Pact to formulate

recommendations in structural terms—except in the case of

program countries, where limited financing makes headline

targets necessarily more binding.

- The pace of underlying fiscal adjustment should not be

changed in response to relatively contained variations in

the growth outlook. This position is consistent with the

long-standing view that fiscal policy is not an effective

instrument for fine tuning the cycle. However, in case of a

major shock to the recovery, fiscal policies may need to be

recalibrated in countries with fiscal space, in the context

of a reassessment of the overall macroeconomic policy mix.

To ensure a timely fiscal response, contingency plans should

be ready, prioritizing temporary revenue and expenditure

measures with the highest payoffs in terms of economic

activity (see the April 2012 Fiscal Monitor).

- The composition of fiscal adjustment should be guided

primarily by the need to foster the economy’s growth

potential over the longer term and by country-specific

factors. Specifically, priority should be given to cutting

spending in countries where expenditure is already high and

correspondingly heavy tax burdens limit the scope for

raising revenues without adversely affecting economic

efficiency and growth. Ideally, cuts should target

unproductive outlays identified through comprehensive

expenditure reviews. Figure 5 illustrates that for most

advanced economies, expenditure restraint is indeed part of

their consolidation plans. Where there is room for revenue

increases, as in the United States and Japan, opportunities

should be exploited to widen bases by eliminating exemptions

and unwarranted special treatment under the tax code rather

than just raising rates. Fiscal policy in many countries can

also be adjusted to better support employment—for instance,

through revenue-neutral reductions in the labor tax

wedge—which would also boost potential growth.8

Some emerging economies (notably Egypt, India, Indonesia,

and Saudi Arabia) could benefit from eliminating fuel and

other subsidies,9

while Turkey, Russia, and South Africa should take measures

to prevent expenditure growth from outpacing the economy’s

medium-term income growth.

- Reforms affecting long-term spending trends remain

important to help strengthen fiscal credibility.10

For advanced Europe, the EC’s recently issued 2012

Ageing Report reiterates the risks to fiscal

sustainability arising from demographic changes. The

Report estimates that over 2010–30, pension costs would

increase by 0.5 percent of GDP, and health care costs by

0.7 percent of GDP. While the pension projections are

broadly consistent with those prepared by the IMF staff,11

the increase in public expenditure on health care is likely

underestimated by about 1 percent of GDP as the cost

pressure arising from technological change is not fully

taken into account.12

However, fiscal policy alone cannot stabilize market

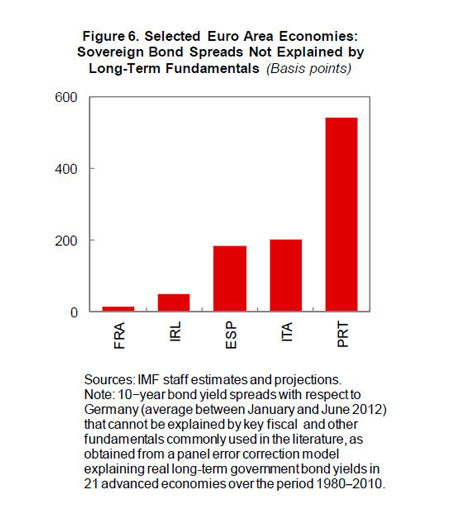

conditions in the euro area. Current sovereign spreads are well

above what could be justified on the basis of fiscal and other

long-term fundamentals (Figure 6), suggesting that wide-ranging

reforms durably affecting expectations—discussed in more detail

in the WEO and GFSR Updates—are needed. In

particular, it will be critical to delink sovereigns’ and banks’

balance sheets. The European leaders agreed at their June summit

upon significant steps to address the immediate crisis, which,

if implemented in full, will help break these adverse links. In

particular, once a single supervisory mechanism is established,

the ESM would be able to recapitalize banks directly. These

initiatives are steps in the right direction, but will need to

be complemented by more progress toward deeper fiscal

integration and a full-fledged banking union. In the meantime,

there has been notable progress in ongoing initiatives to

strengthen fiscal governance in the last few months. To date, 10

of the 25 EU member signatories have ratified the so-called

Fiscal Compact treaty, which mandates the adoption by 2014 of

rules-based national fiscal frameworks capping structural

deficits. The recent adoption by the European Parliament of two

draft regulations aimed at further enhancing fiscal policy

coordination in the euro area (known as the “two-pack”) is also

welcome, and swift approval by the Council would be desirable.

Among other proposals, the two-pack mandates harmonized national

fiscal rules under nonpartisan oversight, establishes common

budget timelines, and enhances surveillance by the Commission.

Nevertheless, these steps would usefully be complemented by

plans for fiscal integration, as anticipated in the report of

the “Four Presidents” submitted to the summit. It is encouraging

that the leaders have asked the Council President to develop

proposals for a more complete union over the next three months.

Ultimately, this could mean sufficiently large resources at the

center matched by proper democratic controls and oversight.

Introduction of a limited form of common debt, with appropriate

governance safeguards, could provide an intermediate step

towards greater fiscal integration. Issuance of such securities

could, at first, be relatively small and restricted to shorter

maturities, and could be conditional on more centralized control

(e.g., limited to countries that deliver on policy commitments;

veto powers over national deficits; pledging of national tax

revenues). Common bonds/bills financing could, for example, be

used to provide the backstops for the common frameworks within

the proposed banking union (see the GFSR Update).

1 IMF staff projections currently include the maximum

amount of the loan in the debt but not in the deficit.

2 The structural budget balance is equal to the

cyclically adjusted balance adjusted for one-off measures. As

one-off measures are typically not included in projections,

structural and cyclically adjusted balances are expected to be

equivalent in 2012–13.

3 Changes to the 2011 deficit compared to the April

2012 Fiscal Monitor reflect a revision to include part

of the bank recapitalizations (already accounted for in the debt

ratio) in the deficit.

4 IMF staff projections in Table 1 are based on

current policies and do not take into account forthcoming

additional measures that will be taken to reach the 3 percent

deficit target.

5 Changes in the cyclically adjusted balance in

2011–12 with respect to the April 2012 Fiscal Monitor

are due mainly to revisions to the estimate of potential GDP.

6 The IMF staff’s baseline scenario incorporates a

1¼ percent of GDP reduction in the structural primary balance in

2013, largely on account of expiring stimulus measures and some

savings in defense spending. The Bush tax cuts and certain other

revenue provisions are expected to be extended fully for at

least one year, while the automatic spending cuts are assumed to

be replaced by other measures over the medium term.

7 Of course, other policies must work in tandem with

fiscal policy to mitigate downside risks to growth and boost

activity and employment in the longer term. These policies are

discussed in more detail in the WEO and GFSR

Updates.

8 See IMF, “Fiscal Policy and Employment in Advanced

and Emerging Economies” (forthcoming).

9 See IMF, “Recent Developments in Fuel Pricing and

Fiscal Implications” (forthcoming).

10 It will be equally important not to reverse

previously introduced reforms. For instance, France has recently

cut back the pension age to 60 for some long-time workers, at an

estimated cost of 0.1 percent of GDP by 2017, fully covered by

higher labor taxes.

11 See IMF, “The Challenge of Public Pension Reform in

Advanced and Emerging Economies,” IMF Policy Paper (Washington,

2011), available via the Internet:

http://www.imf.org/external/pp/longres.aspx?id=4626

12 This issue had already been raised with respect to

the previous Ageing Report; see B. Clements, D. Coady,

and S. Gupta, eds., The Economics of Public Health Care

Reform in Advanced and Emerging Economies (Washington: IMF

2012), available via the Internet:

http://www.imf.org/external/pubs/ft/books/2012/health/healthcare.pdf

|

|